Between Ambition and Delivery: Risk and Opportunity in the UK Defence Sector

By Kaylan Pall

Introduction

The UK’s 2025 Strategic Defence Review (SDR) marks a decisive break from the assumptions that have underpinned British defence policy since the end of the Cold War. Commissioned by the UK Government, the review reflects a growing political consensus that the era of peacetime defence planning is over. After decades of relative underinvestment, the UK now faces a more volatile and contested global security environment, exposing structural weaknesses in military readiness and industrial capacity.

In response, the government has committed to increasing defence spending to 2.5% of GDP by 2027, alongside a longer-term ambition of reaching 3.5% by 2035. This signals not only a fiscal expansion, but a broader strategic repositioning of defence as a central pillar of national resilience and economic policy. As capital flows into the sector and procurement accelerates, the opportunity set for industry is expanding rapidly. However, this shift also introduces a new set of risks that stakeholders must carefully navigate.

The Market

The UK defence market is entering a sustained growth phase, underpinned by rising government expenditure and heightened geopolitical demand. In the 2024/25 financial year, defence spending reached £60.2 billion, with projections indicating an increase to £73.5 billion by 2028/29, equivalent to an average real-terms growth rate of approximately 3.8% per year. This expansion is driven by a deteriorating global security environment, including the ongoing war in Ukraine, intensifying strategic competition with China, and pressure from the United States for European allies to assume a greater share of collective defence responsibilities. At the time of writing, the escalation of conflict involving Iran further underscores the fragility of the global security environment and reinforces the urgency behind renewed defence investment.

Historically, this marks a significant inflection point. UK defence spending has declined as a share of GDP since the post-war period, falling from approximately 7.6% in 1955 to around 2% in recent years. The current trajectory therefore represents a clear break from decades of contraction, signalling a return to sustained rearmament. Structurally, the market is characterised by a small number of dominant prime contractors, supported by a broad and specialised supply chain. At the same time, the composition of demand is evolving. While traditional platforms remain central, increasing investment is being directed towards cyber capabilities, space-based assets, and advanced technologies such as autonomous systems. This shift is reshaping the competitive landscape, opening the sector to new entrants while placing pressure on existing procurement and delivery models.

Government and Procurement

The SDR sets out an ambitious programme of procurement reform aimed at addressing long-standing inefficiencies within the Ministry of Defence. The scale of the problem is evident in its own metrics: for projects valued above £20 million, the average time to contract award stands at approximately 6.5 years. The government has committed to reducing this timeline dramatically, with future procurement cycles measured in months rather than years. Alongside this, the MOD is shifting away from short-term budgeting towards a 10-year Defence Investment Plan, supported by an Integrated Force Plan intended to align capability requirements more directly with funding decisions. Whilst the ambition is clear, there is little evidence that the delivery mechanism has materially improved.

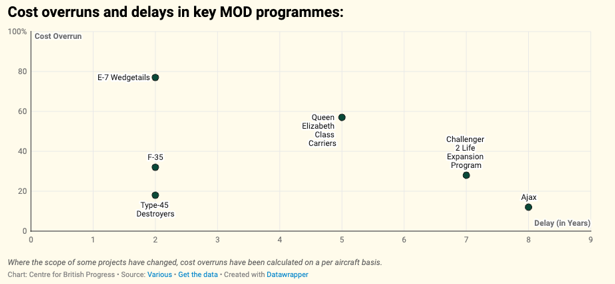

Recent legislative changes have done little to resolve these structural issues. While the Procurement Act 2023 introduced defence-specific exemptions and accelerated procedures, it stopped short of a comprehensive overhaul of a system long criticised for bureaucratic complexity and persistent delivery failures. Cost overruns, driven by in-year savings requirements and the repeated re-profiling of major projects, have imposed significant financial strain on the defence budget. Delays to submarine programmes, alongside the failure to procure replacement frigates in a timely manner, have resulted in substantial additional expenditure, including costly life-extension programmes for ageing platforms. These are not isolated incidents; ongoing technical issues with platforms such as HMS Queen Elizabeth further illustrate a pattern of inefficiency embedded within the system. Figure 1 further illustrates the pattern of delivery failures.

For stakeholders, the central risk lies in the gap between political intent and institutional capability. Commitments to position the UK as Europe’s leading military power must be assessed against a shifting fiscal and geopolitical landscape. Germany’s recent increase in defence spending, now exceeding that of the UK in absolute terms, highlights an increasingly competitive environment. At the same time, rising defence expenditure is placing growing pressure on wider public finances, with non-defence departmental spending expected to remain constrained. Investors are becoming increasingly concerned that the current Labour government’s spending commitments may prove difficult to sustain. This concern is reinforced by recent instances where fiscal pressures have led to the scaling back or postponement of previously signalled spending commitments, suggesting that defence targets may ultimately face similar constraints. While strategic ambition is expanding, the fiscal and administrative capacity required to deliver it remains uncertain.

Industrial Capacity and Supply Chain

The ambitions set out in the SDR rest on the assumption of an industrial base capable of scaling rapidly to meet increased demand. That assumption is increasingly difficult to sustain. The UK defence workforce is ageing, while shortages of highly skilled engineers and technicians are constraining the sector’s ability to deliver complex, high-value programmes. These skills gaps are particularly acute in areas such as nuclear engineering, advanced manufacturing, and digital systems integration, all of which are critical to next-generation defence capabilities.

Supply chain vulnerabilities further compound this challenge. The UK remains heavily dependent on external sources for key inputs, including rare earth elements and advanced materials, with significant exposure to China. This dependence creates strategic risk, particularly in a more contested global environment where access to critical inputs may be restricted. Without greater resilience and, where possible, sovereign capability in these areas, ambitions around advanced systems such as hypersonic weapon and next-generation air defence face clear structural constraints. Whilst these challenges are not unique to the UK, they are reflective of a broader European trend. Defence procurement across Europe continues to be characterised by slow reform and limited innovation, while industrial capacity constraints are already hindering efforts to scale production and strengthen air and missile defence. The UK is therefore operating within a wider system that is itself under strain.

In response, the government has sought to maintain momentum through measures such as expanding the definition of defence spending and increasing reliance on private financing. While these approaches may support headline expenditure targets, they do little to address underlying capacity constraints. For stakeholders, the key risk lies in the divergence between inputs and outputs. Rising budgets do not necessarily translate into deployable capability. The critical metric is not spending commitments, but equipment delivered and operational readiness achieved.

Strategic Dependence on the United States

The UK’s defence posture remains deeply integrated with that of the United States, creating a structural dependency that carries increasing strategic risk. This reliance spans critical areas including intelligence sharing, nuclear deterrence, advanced weapons systems, and operational interoperability. While this relationship has historically underpinned UK military capability, it also exposes the UK to shifts in US political priorities.

The shift towards a more transactional US foreign policy, raises important questions around the reliability of American security guarantees and long-term commitment to European defence. Recent rhetoric emphasising burden-sharing and reduced US involvement in NATO underscores the possibility of a less predictable strategic partner. For the UK, this introduces uncertainty not only in terms of military coordination but also in access to critical technologies and defence collaboration frameworks. This dependency is particularly evident in high-end capabilities, where the UK relies on US systems, components, and integration support. Any disruption to this relationship, whether political or economic, would have immediate implications for operational readiness and long-term capability development.

For stakeholders, the key risk lies in the asymmetry of the relationship. While the UK remains closely aligned with US strategic objectives, its ability to influence US policy is limited. As a result, UK defence planning must increasingly account for scenarios in which US support is conditional, delayed, or reduced. Greater emphasis on European cooperation and domestic capability development may therefore be required to mitigate this exposure.

The Iran Conflict

The SDR’s designation of Iran as a strategic challenge has been overtaken by events. On 28 February 2026, the United States and Israel initiated strikes against Iran targeting its nuclear and ballistic missile programme. Iran’s response, including attacks on Israeli territory, US military bases, and regional infrastructure, marks a significant escalation with direct implications for the UK. The use of UK-linked bases, including Diego Garcia and RAF Fairford, places Britain within the escalation chain rather than at its periphery. The attempted strike on Diego Garcia demonstrates that UK-associated assets are now within the targeting calculus of Iranian strategy, fundamentally altering the UK’s risk exposure.

The strategic consequences extend beyond the region. Disruptions to key maritime routes such as the Strait of Hormuz introduce wider economic and security risks. For the UK defence sector, the conflict compresses already ambitious timelines. Procurement reform measured in years is incompatible with an operational environment that now evolves in days. The case for accelerated spending has never been clearer. Equally, the risk of misallocation under pressure has never been higher.

Conclusion

The UK defence sector presents a compelling opportunity. Political commitment is strengthening, private capital is mobilising, and the strategic rationale for sustained investment is becoming increasingly difficult to ignore. However, the gap between ambition and delivery remains the defining risk. Procurement reform is promised but structurally unproven. Industrial capacity is constrained. Strategic dependencies persist. And spending commitments, however substantial, remain exposed to the fiscal and political pressures that have historically undermined defence policy. The SDR should interpreted less as a as signal of intent. Whether that intent translates into credible military power will depend not on the scale of investment, but on the system’s ability to deliver under pressure.