The Hormuz Effect: LNG Markets and European Energy Security

By Dimitriy Gasilin and Max Leyshon

Section 1: Risk Analysis

The Iran war and its disruption to the Strait of Hormuz remains the largest threat to the global LNG market. Qatar being the third largest exporter of LNG globally, with 18.8% of market share, has an integral role in LNG supply globally and the implications of their exports being cut off for the foreseeable future will be felt across the markets. Since the escalation of the Russia-Ukraine war, Europe has heightened its dependency on LNG with total imports of LNG rising from 127 to 133 billion cubic tonnes between 2022-2023. This trend has continued, with LNG as a share of total gas imports increased from 21% to 45%, with major infrastructure projects boosting capacity by 70 bcm in 2023-2024, with an additional 60bcm expected to become available throughout the next 5 years. Notably the floating storage and regasification units (FSRU) that have recently been announced have been a focus for the EU, offering fast and autonomous storage for countries, mitigating the congestion problems that caused huge gas shortages in 2022 during the advent of the Russia-Ukraine War. Europe's strategic pivot to LNG, while a deliberate move to secure long-term energy independence, now carries significant downside risk — the Iran conflict and closure of the Strait of Hormuz threaten to expose the continent to sustained price volatility.

Reliance on US LNG: Implications

The US has led investment into liquefaction capacity, accounting for 55% of the final investment decisions on export capacity, compared to Qatar which recorded 15% since 2019. Europe has not only maintained its reliance on US LNG imports but is now its core customer. Dependency on the US has been increasing from 41% in 2022 to 56% in 2025, while the share of LNG from Qatar almost halved from 15% in the same period. Europe’s declining dependency on Qatari LNG and appetite for US as its dominant supplier, is a trend that the Middle Eastern conflict has intensified, as across March 2026, 64% of US exports went to Europe, demonstrating the importance of US LNG on EU energy supply.

A bilateral trade deal has set the basis for a commercial framework in which the EU is close to agreeing on a commitment to purchase $750 billion of US energy exports up to 2028 in exchange for partial tariff immunity. Europe’s supplier concentration risks have shifted from the unpredictability of reliance on Russia to a new dynamic in which dependence on the United States may enhance Washington’s leverage over the transatlantic trade and political cooperation beyond 2025 agreements. The US supply portfolio follows a free on-board approach, allowing Europe to use US LNG as a buffer against energy security challenges, reinforcing the deep positioning of this supply route within its strategic energy framework. For European investors, provided Washington’s terms remain moderated by close political ties, the United States offers a flexible alternative fuel supplier. This allows Europe’s shift away from Russian energy and provides a margin to meet autumn gas refill targets but also reinforces a new dependency carrying longer-term strategic implications.

Europe is now exposed to price increases attributable to extreme weather conditions, including winter storm events. Winter Storm Fern in January 2026 led to Henry Hub spiking to a historical high of USD 30.72/MBtu, leading to a sharp rise in import costs for Europe during a period where the continent’s energy demand surged to 33% in the aftermath of Storm Goretti. Future weather pattern alterations induced by climate change are expected to cause more frequent severe storm events across the Atlantic, leading to the redirection of LNG towards domestic consumption in the US, along with trade routes disruption. As seen in January, this would place Western and Northern Europe in a position that undermines energy security, as governments may draw down underground storage, while intensifying competition with Asian buyers for tightening spot cargo availability.

The EU own goal of ‘diversifying energy supplies’ contradicts H1 2025 data indicating a combined US and Russian LNG import share of 70%. Simultaneously, repeated violations of Clean Air Act standards at US export terminals pose a direct challenge to Europe’s low-carbon strategy and its autonomy in selecting cleaner energy sources. A key consideration is whether the efforts of individual EU member states to secure their own energy supplies and autonomously diversify their energy mix will outpace the expanding reliance on US LNG.

EU’s FSRU reliance during Strait of Hormuz Crisis

Scenario: The Strait of Hormuz chokepoint persists across summer months.

Across Q1 2025, 52% of LNG flows through the Strait of Hormuz were destined for China and India, each receiving volumes of up to 2.5 billion cubic feet per day (Bcf/d). European destinations received significantly lower volumes at 1.4 Bcf/d, half of this allocated to Italy’s LNG purchases. The closure of The Strait of Hormuz prolonging into summer will continue to tighten supply of both Gulf and non-Gulf LNG, even under current falling demand trends across Europe and Asia. Europe risks losing flexibility in obtaining supplies for winter storage due to fiercer bidding in LNG spot markets. A risk assessment of two countries where FSRUs act as a key entry point is necessary to gauge how well national and regional supply is insulated from changing spot market dynamics.

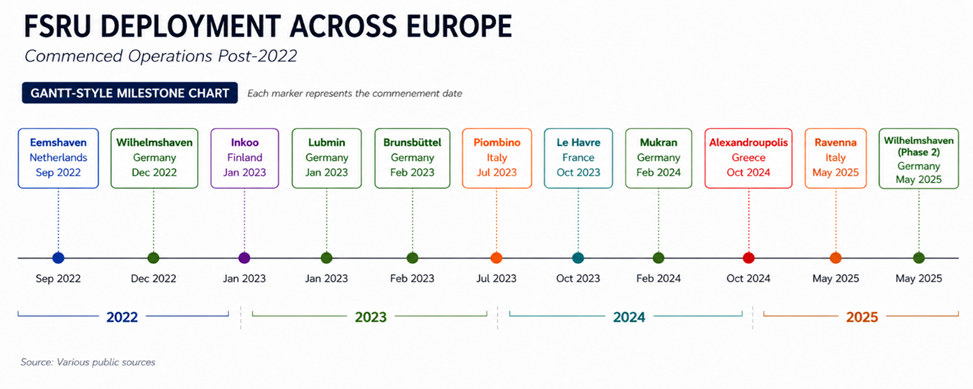

Figure 1: FSRU Deployment across Europe. Terminals that commenced operations post- 2022. Source: IEEFA and other various open public sources and reports.

The EU incorporates meeting gas storage targets into its wider energy security framework, with gas fuelling approximately a third of its winter gas consumption. Under amended Gas Storage rules 2025-2027, member countries follow a 2-month window between 1st October - 1st December to reach a 90% filling target, subject to market conditions and technical constraints. Under the RePower EU plan, European countries have accelerated investment into FSRU’s since 2022 as a solution to reduce dependence on Russian gas and diversify energy supplies through increased LNG import capacity. Between 2021-2025, EU’s total LNG import capacity rose by 76bcm to a total capacity of 242bcm/ per year. Ramping up capacity through FSRU’s bypasses longer timelines, as standard onshore LNG terminal projects require a development phase of up to 5 years (2 - 3 if fast-tracked), while converting a vessel unit into an FSRU can be undertaken 1 - 2 years.

Single-point dependency

A Hormuz Strait crisis scenario tests overall resilience of EU members, however especially those susceptible to single-point dependency. Risks emerge when geopolitical uncertainty and market volatility threaten FSRUs critical role in a country’s gas import supply chain. These risks materialise in lieu of onshore terminal infrastructure, compounding if lost volumes are irreplaceable through pipeline gas. A country using FSRUs to meet temporary spikes in demand differs in its risk exposure from a country relying on timely send-out via its key FSRU project, especially if regional implications are tied to supply shocks. Lithuania offers a useful analytical lens for examining single-point dependency risks in a region that has made concerted efforts to eliminate Russian gas flows entirely. Lithuania’s Klaipeda LNG terminal acts as the country’s sole entry point for LNG volumes and is critical to securing both domestic and regional demand. Unlike Finland’s Inkoo terminal, Klaipeda remains ice-free, which has enabled it to experience high market demand for long-term regasification capacity bookings until 2033.

In H1 2025, 60% of Klaipeda’s gas imports were exported to Lithuania, Poland, Latvia and Estonia, feeding satellite LNG terminals around the Baltic Sea region. Since Klaipeda LNG terminal became operational in 2014, 52% of its LNG came from Norway and 37% from the United States, with deliveries also recorded from partners around Africa (Nigeria, Egypt, Algeria) and the Caribbean (Trinidad and Tobago). In 2025, the share of gas delivered from the US stood at 69%, in comparison to 25% arriving from Norway. As reported by KN Energies, Klaipeda’s largest-ever delivery came from the US in April 2025. This serves as a strong, though not standalone, signal that future shipments and contracts may align with Europe’s expanding transatlantic reliance, heightening its exposure to geopolitical friction scenarios and US supply-side price spikes. Although 11% of its supply portfolio is spread primarily among non-gulf-LNG players, Klaipeda’s ability to secure non-contracted supply during a crisis depends on continued summer demand interest, including allocating those slots which have been reoffered to market participants. Up to 2TWh of its regasification capacity is available between June - August 2026, coinciding with the EU’s summer gas injection season.

Figure 2: Graph showing utilisation rates across FSRU terminals in the EU. Data provided across H1 2025

Klaipeda LNG is positioned well to meet domestic demand, with an estimated nominal regasification capacity of 2.77 billion, which in Q1 2025 provided 84% of the total gas transported into Lithuania’s energy grid. In Q1 2026, consumption of gas in the Baltic region has risen by 29%, due to unusually cold spells, as Lithuania observed a 20% increase in demand up from around 5.6TWh in Q1 2025 to 6.8TWh in January - March 2026. Klaipeda’s utilisation rate averaged at around 92% in Q1 2026, significantly higher than its 68% full-year average in 2025, although the comparison is influenced by seasonal demand fluctuations.

Under the current crisis scenario, Lithuania’s Baltic partners are expected to intensify their draw on Klaipeda, with Latvia’s underground fill level at 26% at the beginning of May 2026, lower than EU’s total of 33%. The terminal’s risk exposure has heightened, as Latvia’s peak withdrawal for 2026 stands at 190GWh/d, compared to 152GWh in 2025. Given Lithuania’s own refill obligations, a risk emerges around whether the terminal, recently operating near maximum capacity, can allocate capacity effectively during a rush to hedge against geopolitical uncertainty while meeting multiple regional pressures simultaneously.

SECTION 2: Market Analysis

TTF Snapshot

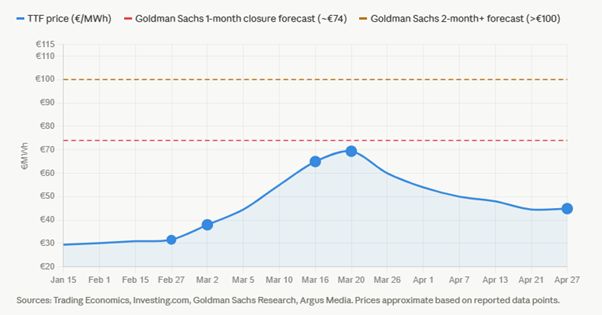

The Title Transfer Facility is Europe’s main gas benchmark, since the Iran conflict, the TTF has responded sharply, reinforcing the pre-war assessment that Europe would be highly sensitive to disruption in the Middle East. The price response was compounded by historically low storage levels due to a harsh 2025 winter in Europe, resulting in only 46 bcm in storage by the start of March.

The announcement of the war led to a 20% spike in the TTF in one day, with the price being around €32/MWh pre-war and spiking to a peak of €69/MWh in mid-March. With no end in sight to the disruption, the TTF remains buoyant with the price around €44/MWh at the tail end of April.

Long-term Gas Contracts: The Fallacy of Protection

A long-term gas contract locks in gas supply and a set quantity for a long period of time, typically 10 or 20 years. This guarantees countries like Germany, whose federal government have a contract at Wilhelmshaven, that they will receive gas no matter the global conditions, meaning they have secured vessels, the infrastructure and a supply stream of LNG for the contract duration. Although this seems beneficial, especially as Germany are moving away from reliance on Russian gas, the long-term contract agreement does not protect them from price fluctuations, as the price of the gas is often pegged to the TTF price.

The issue here is Germany has a huge industrial base that relies on this gas for power, and unlike residential gas prices which may often be subsidised, heavy industry firms are not protected in the same way and will be forced to pay the inflated wholesale gas prices. This is expected to cause inflationary pressure in Germany and other industry heavy European nations.

For context, during the height of the European energy crisis in the wake of Russia’s invasion of Ukraine in 2022, the TTF hit heights of €200/MWh, this caused German industry to grind to a halt as the cost of energy was simply untenable. As of the end of April this is not the case, however, if the Strait of Hormuz remains shut and Qatar’s Ras Laffan remains shut, the TTF is expected to rise. As per Goldman Sachs, TTF gas prices could exceed €100/MWh – meaning the cost of energy will have tripled for European industry. Consequently, the issue with Europe and energy is not one of supply, but of the effects of global supply disruption on the price of gas.

Spot prices: Bidding War

The IRGC's closure of the Strait of Hormuz has, overnight, removed 20% of global LNG supply from the market and reduced available LNG carrier capacity by 2.5%. Pre-war, Qatari LNG was mainly bought by the Asian market – roughly 83% of their LNG exports and are priced at a premium using the JKM rather than the TTF benchmark, specifically countries such as Japan and South Korea are used to paying higher prices for LNG from Qatar due to their reliance on Gas for their power.

This has culminated in a bidding war for the unaffected LNG supply, mainly from the US basin. The issue for Europe is that spot prices are now inflated, and the Asian buyers are willing to pay more for LNG, this has created an environment where not only are gas prices now higher but also a bidding war has started between Europe and Asia for these shipments from the US. The suppliers from the US will act in their commercial best interests, and if the JKM is trading above the spot price of the TTF, Europe will be without LNG supply at the spot rate. This seems like a small issue, however the longer the Strait of Hormuz remains shut, the more aggressive the bidding war will be and both the TTF and JKM will be expected to rise. This effect will become more pronounced in Q3 as the spread between the JKM-TTF widens as the two areas prepare to fill storage for the winter – the longer the Hormuz remains shut, the larger this effect will compound and will likely drive LNG prices even higher than expected. This will further damage Europe’s energy supply as only long-term contracted LNG deals will hold, and even then, prices may reach similar levels to the 2022 crisis and be untenable for European industry.

The Congestion Resolution

A distinct difference between the 2022 European energy crisis and the closure of the Hormuz is Europe has now adapted to LNG. A critical reason for the astronomical prices of gas in Europe in 2022 was the congestion caused by the lack of regasification infrastructure, leading to delays in receiving gas, due to pipeline interconnectors running at maximum capacity. This has been resolved since 2022 and Europe has the storage capacity to handle rises in LNG demand, this has eliminated the TTF premium that existed in 2022, and it can be expected will shorten the JKM-TTF spread compared to previous crisis levels. The implementation of the aforementioned FSRUs has helped solve this problem and demonstrates Europe’s commitment to LNG as a key part of the EU’s energy security framework.

TTF-JKM Spread Analysis

Due to the congestion problem being resolved, it is expected that the TTF will not trade at a premium compared to the JKM during this scenario compared to 2022. However, initially after the start of the Iran war, the TTF spiked above the JKM at $19/MMBtu compared to the JKM $13.5/MMBtu at its peak spread. This demonstrates how Europe was faster to reprice the Qatari supply loss whereas Asian buyers predicted that the disruption would only be temporary. Since this initial price action, the JKM has started trading above the TTF with a $1.86/MMBtu premium, showing how Asian markets are now realising the loss of Qatari LNG supply is no longer a short-term event.

Furthermore, the market has this premium to be narrowing as we head towards Q3, with this premium falling to $1.10/MMBtu for July delivery, reflecting how competition between Europe and Asia for LNG will worsen as replenishing reserves for winter 2026 begins.

There are varying predictions around when and if the Strait of Hormuz will open, however one thing is for certain, and this is - the longer the straight is closed, the worse the impact will be for LNG importers. Even a conservative prediction of a one-month closure will lead to a serious surge in spot prices for both TTF and JKM. Goldman Sachs has predicted that a one-month closure would lead to an increase in spot prices from around $15/MMBtu now (in both), to highs of $24/MMBtu in July for TTF and $20/MMBtu for JKM – a 60% increase and 33% increase respectively. The spread would be unlike the traditional JKM premium and would be inverted towards a long-lasting TTF premium until about October when they expect parity in the spread.

However, the more likely scenario, is this closure is not short-term and cannot be quickly fixed. The IRGC has shown no change in stance so far and remains steadfast in their position. This dynamic implies a closure for the foreseeable future is likely, this has vastly different implications compared to a short term one month closure. The largest difference is the price of spot at both benchmarks, with predictions of highs of $33/MMBtu for the TTF in July at its peak and then a peak in the JKM of $30/MMBtu in August. This would be a doubling of gas prices compared to current rates of today in April, interestingly the TTF would initially trade at a premium compared to the JKM, but this would be expected to invert in August as gas prices become unaffordable for Europe and heavy industry will cut back on production – as seen in 2022. Asian demand for gas is structurally less elastic, given the region's heavier reliance on it as a primary energy source, whereas Europe retains the flexibility of alternative low-carbon energy sources.

Impact on Shipping

Since 2022, Europe gets most of their LNG from the US, with European demand making up 72 million tonnes of US LNG exports compared to Asia’s 19.6 million tonnes of demand in 2025. Even when the JKM trades at a premium, the extended tonne mileage from the US Gulf to Asia offset the difference in price for Asian importers, hence Asia usually got their gas from Ras Laffan in Qatar. Now, due to the loss of Qatari LNG in the market, US LNG is the key to global supply and spot freight rates have responded accordingly.

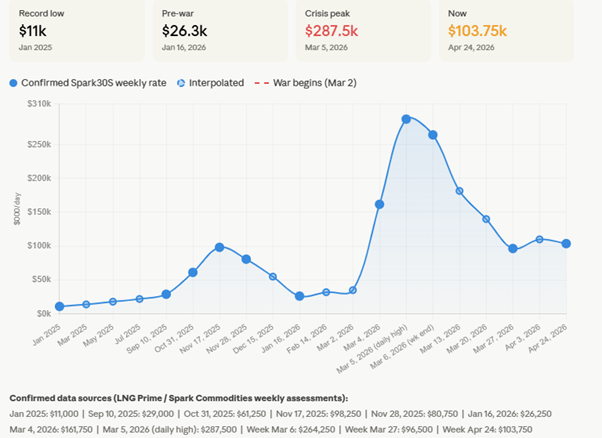

Graph showing US-Europe LNG Freight Rates

Although pre-war rates were very low, the data demonstrates how demand pressures are seriously impacting the cost of LNG freight for charterers importing to Europe. The initial shock of the war made rates react violently as charterers panicked, since this, rates have fallen but still remain buoyant at roughly four times pre-war rates. This reflects ship owner’s realisation that we are in a sellers’ market, and the global disruption of Qatari LNG means they can charge a premium. As the duration of the war still remains unknown, it could be argued these rates are still under priced, especially as we can expect the LNG market to pick up again in Q3 as Europe prepares for winter. This is a win for owners such as Flex LNG who operate a fleet of 13 modern two-stroke LNG carriers and Hoegh Evi who also have a significant presence in the LNG market to Europe.

However, the stabilisation of rates may fall, the main factor here is the market pre-war already had a large surplus of vessels, with an orderbook of 343 vessels against a total of 823 vessels in the market, meaning we can expect an oversupply in the market. This reality, coupled with the loss of 20% of the market as Qatari LNG has been taken offline, means there will be more vessels than ever competing for less freight. Based on this, we can expect to see rates dampening as these new vessels come into the market and the power within the market invert as it becomes a buyers’ market, forcing rates down – potentially below the record lows of $11,000 a day. Some owners have already realised this reality as LNG carriers have been scrapped prematurely at 25 years rather than 38 years, implying this is a long-term structural issue within the market and will not have a short-term fix. Thus, a bullish view on LNG freight rates is likely misinformed.