Pharma industry in France - Market Performance and Industry Risks

By Dmitriy Gasilin

Introduction

Despite continuing dominance from the North American market marked by its 54.8% share of the global sales, the European pharmaceutical industry is dedicated to being visible on the global stage. Europe’s share of sales is 22.7%, almost double China’s share which stood at 7.1% at the end of 2024. Amongst the German and Swiss pharmaceutical giants, France’s success in the industry is especially noteworthy for investors.

France’s health expenditure as a share of GDP in 2024 was 11.5%, placing it 5th globally. France also has the lowest annual growth in health expenditure per capita across OECD members, remaining true across 2014-2019 and 2029-2024 periods. Price levels in France’s health sector are 32% lower than the OECD average, standing out from the UK’s 3% higher than average level and USA at 52% higher than average level. France’s commitment to be a regional leader is supported by an overarching policy vision - ‘Choose France for Science’, with the French Government already unlocking up to €50 million in capital grants in an effort to maintain the country's competitiveness in the industry.

Market analysis

Foreign direct investment in France’s life sciences industry is 162% higher in 2023 than in 2021. In 2024, an example of a major investment totalling €1.87B was revealed by three industry giants - Sanofi, Pfizer and AstraZeneca, aimed at upgrading production facilities and significantly enhancing France’s Research & Development (R&D) capacity. According to WHO statistics France has undertaken 555 more clinical trials in 2024 than in 2023, thus retaining a strong position as a leading European country in clinical trials research. Production is starting to see an improved outlook, helped by a return to a trade surplus of €4 billion in pharmaceutical products according to 2024 trade flows.

Notably, France's main pharmaceutical giant Sanofi has experienced robust sales growth, achieving 13.3% in Q4 2025 at constant exchange rates (CER), and reaching total net sales of €43,626m across the financial year. Sanofi’s sales in Europe grew by a modest 1.6% at CER, compared with a significant 16.3% increase in the United States, and a slightly higher 2% increase in China. When magnifying these increases across Q4, sales in Europe are even less significant, growing at only 0.2%, compared with growth of 22.6% in the US and 6.2% in China.

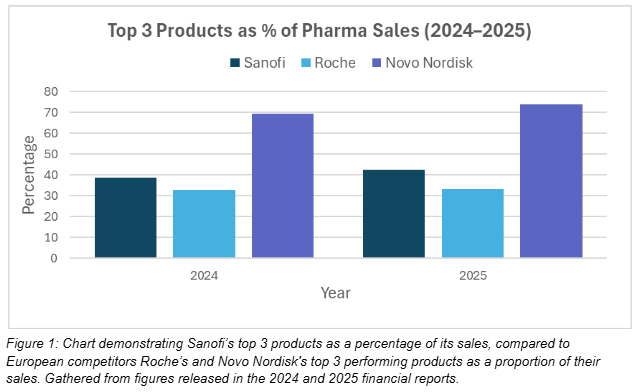

In Figure 1, Sanofi’s concentration of sales between their top 3 products is higher than Roche’s in both 2024 and 2025, increasing from 39% to around 43%. Roche’s top 3 products consist of around 33% of their sales in both years, indicating a heavier reliance on the rest of their portfolio. Novo Nordisk stands out, due to their significant reliance on their top 3 products for their pharmaceutical sales, led primarily by a drive in sales of their Ozempic medication. Pharma launches have contributed to a more concentrated product mix for Sanofi, driven by a colossal rise in sales of the ‘ALTUVIIIO’ treatment to the US, totalling over $1 billion. Sanofi’s net sales from pharma launches growing from 6.93% of its net sales to 8.96% across 2025 is a cautious indicator of its wager on innovation and R&D paying off, contingent on Sanofi prioritising a disciplined launch execution strategy.

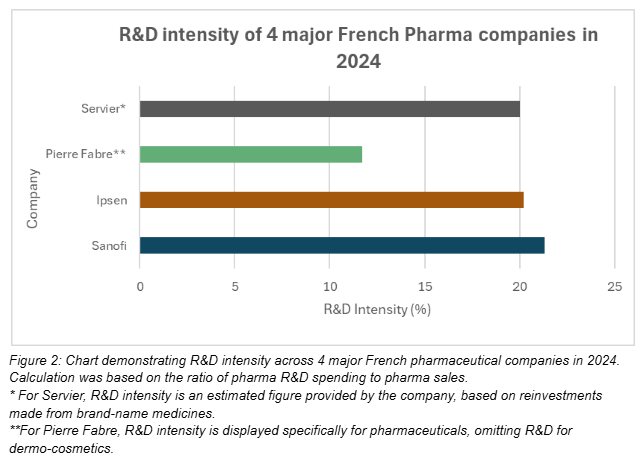

In Figure 2, R&D intensity across 4 major French pharmaceutical companies varies according to size, business focus and degree of innovation. Industry leader Sanofi reached an R&D intensity of 21.3% in 2024, however despite having over €35 billion less in sales, Ipsen’s R&D expenses are not far behind at 20.2%. Servier’s figure also reflects its commitment to R&D, dedicating around 20% of its sales from brand-name medicines towards innovation. Pierre Fabre divides its operations across two areas - pharmaceuticals and dermo-cosmetics, but has reinvested over twice the amount of money from sales in pharmaceuticals compared to dermo-cosmetics, at €155 million versus €64 million respectively. Overall, these figures reflect wider European trends, whereby R&D intensity across Europe’s biopharmaceutical sector was estimated to be at 22% in 2021, lagging behind the USA at 34%, but slightly ahead of the Asia/ Pacific region at 20%.

Qualitative metrics reported through PwC/ LEEM surveys shine a contrasting light on sector performance, with the attractiveness of France’s R&D remaining unchanged across from 2023 to 2024. A justification for this outlook is a concern over France losing its competitive edge to Spain and Germany’s R&D initiatives by means of enhancing clinical trial testing capabilities through decentralisation and acceleration of administrative procedures. Regulatory hurdles have caused a 6% drop in the availability of new medicines that have gained authorisation, already placing France behind Germany, Italy and Spain. A knock-on effect has been exerted on access to medicines, whereby the duration between a medicine being granted a Marketing Authorisation license and it becoming available to patients takes nearly 450 days longer than in Germany and over 100 days longer than in Italy.

Market Risks

France is currently depending primarily on EU imports of pharmaceutical products, having imported 75% of such goods from fellow EU states (7). France’ imports from China have decreased by 32% between 2022-2024, however its share of imports from the United States has crept to 15%, propelled by rising dependence on American innovative medicines. With France exporting around $4 billion worth of pharmaceutical products to the United States in 2024, Trump’s July tariffs levied on EU goods including pharmaceutical products carry an estimated annual loss of up to $19 billion, although the effects could have been far more devastating had the bloc failed to negotiate its position.

Room for negotiating more favourable trade terms is possible, as demonstrated by Sanofi’s deal with the US administration, where the French industry leader has secured a three-year exemption from Section 323 tariffs on exports to America, in return for reaffirming a commitment to invest $20 billion in US-based production, alongside a price freeze for treatments via Medicaid at a rate charged to other high-income countries. An immediate downside to such agreements is an opportunity cost associated with investing in upgrading facilities in America rather than France. However, Sanofi’s financial statements convey a growing reliance on the US market, especially for their blockbuster ALTUVIIIO, therefore complacency cannot be afforded. French and European companies have limited options aside from agreeing on terms favouring US authorities, with GSK and Novartis announcing similar deals, both pledging investments of $30 billion and $23 billion, respectively.

Tackling dependency on external supplies is a collective challenge facing Europe. Production being concentrated in India and China is a factor, however according to the European Commission's own research, more than 50% of medicine shortages have been caused by manufacturing issues, and unforeseen demand causes 16.7% of the stockouts. In France, data from 2022 indicated insufficient production capacity to be the leading cause of drug shortage at 27.1%. This data ties in with France’s limited role in pharmaceutical manufacturing, having hosted fabrication sites for fewer than 10% of the 431 medicines approved in Europe since 2020, thus falling behind Poland, Spain, and Ireland. Despite France increasing its raw production of pharmaceutical preparations to around 8% above 2021 levels as of autumn 2025, both national and EU-wide research into supply shortages suggest more domestic action is required to avoid critical disruption.

The Critical Medicines Act is the EU’s latest major proposal to curb dependence on global supply chains in favour of securing regional stockpiles and mitigating vulnerabilities. Under such proposals, procurement will have to factor in supply chain shocks and level of interdependence on non-EU suppliers, instead of a business model centred solely around cost competitiveness. For ‘critical’ medicines, domestic supply would gain priority for procurers, signalling a crucial movement towards protectionism in the pharma industry, although exposure to competition within the Union will likely remain for French companies.

Sanofi’s innovation may also instill optimism for investors, especially since the launch of Euroapi - a European company focused on R&D and marketing of active pharmaceutical ingredients (API’s) . Sanofi’s goal with this venture was offsetting reliance on imports which have reached rates of up to 100% for API’s imported from India and China. The company commands a portfolio of 200 APIs since spinning out from Sanofi, however its recent half year financial report suggests a downturn in net sales from €448.7 million in June 2024 to €412.1 million in 2025.

Conclusion

France’s R&D and clinical trials sectors look at risk from European competitors, however analysis of company expenses demonstrate that R&D intensity for 3 out of the 4 major French companies is on par with the European average. Potential investors should consider regulatory risks resulting in a prolonged timeline of getting their product to the patient. While production seems to have improved over the last year, previous data indicates insufficient capacity as a core challenge that halts the industry. Implications from US tariffs are not yet apparent, however French and European pharma corporations pledging billions in US investments can hardly be considered a positive sign for both the French government or domestic stakeholders. The EU's Medicine Act framework offers an opportunity to increase demand for French products if signed, although it does not eliminate competition from fellow EU companies.